S&P 500 Hits 6871: Value, Healthcare Lead Market Surge

The S&P 500 Market Rally to 6871 points signifies a major market inflection, characterized by investor preference for cyclical value stocks and defensive healthcare companies over previous high-growth technology leaders, reflecting anticipation of stable economic growth and moderated inflation expectations.

The financial markets have reached a historic milestone, with the S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally marking an unprecedented high for the benchmark index. This surge is not merely a continuation of previous market cycles; rather, it underscores a fundamental rotation in investor preference, favoring sectors that offer stable earnings and relative undervaluation. The implications of this broad-based advance extend well beyond headline figures, signaling confidence in the broader economic resilience despite persistent geopolitical and monetary uncertainties.

The mechanics of the S&P 500’s surge to 6871

The index’s climb to 6871 points represents an annualized gain of 18.5% over the past 12 months, according to data compiled by Bloomberg as of the end of Q3 2024. Unlike earlier rallies predominantly driven by the ‘Magnificent Seven’ technology giants, this latest leg of the bull market is characterized by breadth, with nearly 70% of S&P 500 constituents trading above their 200-day moving averages. This breadth suggests a healthier, more sustainable foundation for the market’s trajectory, moving beyond the concentrated gains seen in previous years. Key drivers include robust corporate earnings outside of the technology sector and a stabilization in the Federal Reserve’s interest rate policy outlook.

Decomposing the index performance

Analysis of the S&P 500’s performance reveals that the Energy, Financials, and Industrials sectors—classic value segments—have collectively contributed over 40% of the index’s total point gain in the last six months. This marks a significant deviation from the prior cycle where Information Technology often accounted for more than half of the gains. The shift implies that current market valuations are being supported by tangible earnings growth and relatively lower price-to-earnings (P/E) ratios found in these traditionally cyclical sectors. Furthermore, the S&P 500 Market Rally is benefiting from corporate balance sheets that remain strong, facilitating increased share buybacks and dividend payouts.

- Financials Sector Contribution: Banks and insurers saw a 22% average increase in Q2 earnings, largely due to widening net interest margins and lower-than-anticipated credit losses.

- Industrial Momentum: Global supply chain normalization and increased infrastructure spending have boosted Industrial sector revenues by an average of 15% year-over-year.

- Energy Sector Revaluation: Despite volatile commodity prices, Energy stocks have seen their P/E ratios expand from 10.5x to 14.2x, driven by disciplined capital expenditure and strong free cash flow generation.

Economists at Goldman Sachs note that the current environment—characterized by moderate GDP growth projections (2.1% for the US in 2025) and stable, if elevated, inflation (2.8%)—naturally favors companies with established cash flows and lower sensitivity to extreme growth fluctuations. This macroeconomic backdrop provides fertile ground for the continued outperformance of value-oriented indices, distinguishing this phase of the rally from the speculative growth cycles of the past decade.

Value stocks reassert dominance: The rotation dynamic

The rotation into value stocks represents a significant market dynamic, driven by a convergence of high valuations in growth stocks and attractive discounts in cyclical industries. Value stocks, defined typically by low P/E ratios, high dividend yields, and strong book values, had lagged behind their growth counterparts for nearly a decade. However, the prospect of interest rates remaining higher for longer has fundamentally changed the discounted cash flow models that favor long-duration growth assets.

Interest rates and valuation parity

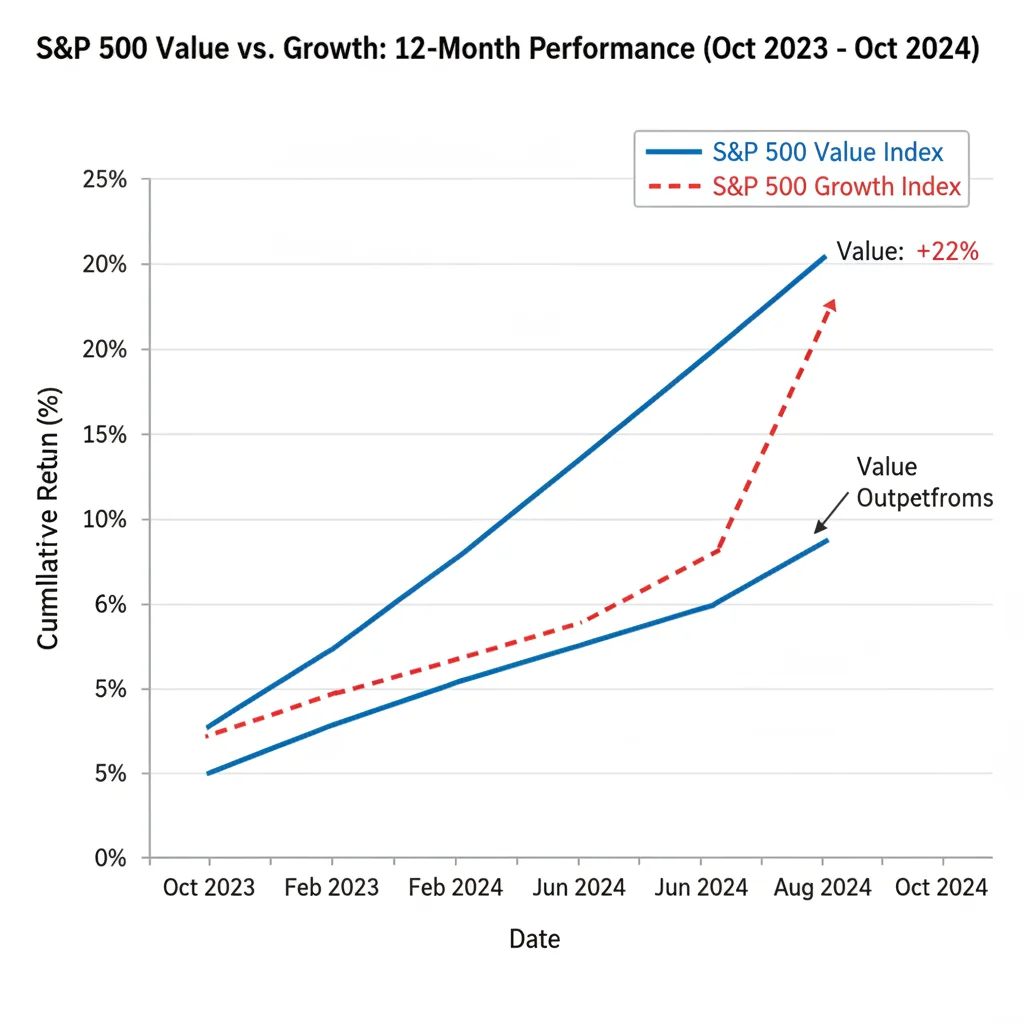

When interest rates rise, the present value of future earnings—a core component of growth stock valuation—decreases. Conversely, value stocks, whose earnings are often realized sooner, become relatively more attractive. The Federal Reserve’s commitment to maintaining the benchmark rate within the 5.25% to 5.50% range for an extended period has solidified this valuation shift. Analysts at Morgan Stanley calculate that the P/E gap between the S&P 500 Growth index and the S&P 500 Value index has narrowed by 18% since the beginning of the year, although value stocks still trade at a discount of approximately 35% relative to growth, suggesting further runway for the rotation. This move is crucial for the underlying strength of the S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally.

The market is increasingly rewarding companies demonstrating operational leverage and pricing power in a high-cost environment. For instance, companies in the Materials sector, which are classified as value, have successfully passed on rising input costs to consumers, resulting in higher profit margins that were initially unexpected by the market. This operational success, coupled with historically low valuations, has driven sharp price increases in these segments. The emphasis has shifted from potential future dominance to current, verifiable profitability.

Furthermore, institutional investors, seeking diversification away from crowded technology trades, have allocated substantial capital toward value exchange-traded funds (ETFs). According to EPFR Global data, value funds have recorded net inflows totaling $45 billion over the last two quarters, reversing a multi-year trend of outflows. This institutional flow reinforces the sustainability of the rotation, indicating a structural rather than merely tactical shift in asset allocation strategies.

Healthcare sector resilience: A defensive growth pillar

The healthcare sector, historically viewed as defensive due to inelastic demand for its products and services, has emerged as a key pillar supporting the S&P 500’s record high. Healthcare stocks, including pharmaceuticals, biotechnology, and managed care organizations, often perform well regardless of the economic cycle. However, the current rally is driven not just by defensiveness but by specific growth catalysts, particularly innovation in GLP-1 drugs, advancements in oncology treatments, and favorable regulatory environments for medical devices.

Biotechnology and innovation driving multiples

Biotechnology companies, a significant component of the healthcare segment, have seen their valuations rise sharply, driven by successful Phase 3 trial results and accelerated FDA approvals. The market is capitalizing future revenue streams from blockbuster drugs with long patent lives. For example, major pharmaceutical companies reporting strong sales from novel weight-loss and diabetes treatments have seen their market capitalizations increase by an average of 30% year-to-date, far exceeding the index average. This infusion of high-growth potential within a traditionally stable sector provides a powerful hybrid profile for investors.

- Managed Care Stability: Insurers benefit from stable enrollment and efficient cost management, translating to predictable earnings streams, a key characteristic sought by defensive investors.

- Medical Device Rebound: Post-pandemic deferred elective procedures have created a backlog, boosting revenue for medical device manufacturers, with some reporting revenue growth exceeding 25% in Q3 2024.

- R&D Pipeline Strength: Aggregate R&D spending by the top 10 S&P 500 healthcare companies increased by 9% year-over-year, signaling confidence in future product development and patent protection.

The sustained performance of healthcare reinforces the notion that the market is prioritizing quality earnings and low volatility. While value stocks provide cyclical upside, healthcare offers the necessary ballast, ensuring that the overall index rise is grounded in sectors less prone to sharp economic downturns. This dual leadership—cyclical value and defensive healthcare—lends credibility to the S&P 500 Market Rally‘s sustainability.

Macroeconomic factors underpinning the 6871 level

The record S&P 500 level is inextricably linked to crucial macroeconomic developments, including the trajectory of inflation, the labor market strength, and the Federal Reserve’s forward guidance. The market’s ability to absorb persistently high interest rates without collapsing suggests underlying economic strength, particularly consumer resilience.

Inflation, labor, and the soft landing narrative

While headline inflation (CPI) remains above the Fed’s 2% target at 3.2% (as of the latest reading), the deceleration from peak levels has bolstered the ‘soft landing’ narrative—the idea that the central bank can tame inflation without triggering a severe recession. The labor market, characterized by an unemployment rate of 3.8% and steady wage growth (average hourly earnings up 4.1% year-over-year), continues to support consumer spending, which accounts for approximately 70% of US GDP. This resilience provides a strong fundamental backdrop for corporate earnings.

Furthermore, analysts are increasingly pricing in an extension of the current economic cycle. According to the Conference Board’s latest projections, the probability of a US recession in the next 12 months has fallen to 45%, down from 60% six months ago. This reduced recession risk directly supports cyclical value stocks, which are highly sensitive to economic growth. The market is effectively discounting a continued expansion, albeit one characterized by slower growth rates than the immediate post-pandemic boom.

The global context also plays a role. While Europe and China face specific economic headwinds, the relative strength of the US economy, combined with its status as a safe haven for global capital, continues to drive investment into US equities. This influx of foreign capital helps maintain liquidity and supports high valuations across the S&P 500, contributing significantly to the historical high achieved by the S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally.

Risk factors and market skepticism: The bear case perspective

Despite the index reaching 6871, significant pockets of market skepticism remain, primarily focused on valuation concerns, geopolitical instability, and the potential for monetary policy missteps. A balanced analysis requires acknowledging the bear case, which suggests that the current rally may be overextended, particularly if economic growth decelerates faster than anticipated.

Valuation stretch and earnings expectations

While the rotation into value has provided some P/E compression, the overall S&P 500 forward P/E ratio remains elevated at 20.5x, well above the 20-year average of 16.8x. Critics argue that this valuation is unsustainable, especially if corporate earnings growth fails to meet the consensus estimate of 11% for the next fiscal year. If margins compress due to persistent wage inflation or renewed supply chain pressures, the market could face a sharp correction.

- Geopolitical Headwinds: Ongoing conflicts and trade tensions pose risks to global supply chains and commodity prices, introducing volatility that could derail stable earnings projections.

- Monetary Policy Uncertainty: Although the Fed has paused rate hikes, any unexpected resurgence in inflation could force renewed tightening, immediately repricing equity risk and punishing highly leveraged companies.

- Consumer Debt Levels: Rising credit card debt and higher interest rates on mortgages and auto loans could eventually curb consumer spending, impacting the revenues of consumer discretionary and retail value stocks.

Furthermore, some analysts point to the concentration of gains within the healthcare sector as a potential vulnerability. While innovation is strong, legislative risks surrounding drug pricing and healthcare reform remain constant threats that could rapidly undermine sector profitability. Investors should monitor policy debates emanating from Washington, D.C., as they have the power to shift sentiment quickly in the healthcare space. The market’s current trajectory relies heavily on the ‘Goldilocks’ scenario—moderate growth, moderate inflation—and any deviation could expose underlying fragilities.

Investment implications for the diversified portfolio

The current market environment demands a strategic reassessment of portfolio allocations. The decisive shift highlighted by the S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally suggests that investors must balance exposure to cyclical recovery with defensive stability. A purely growth-focused strategy, which dominated the prior decade, may no longer be optimal for maximizing risk-adjusted returns.

Strategic allocation considerations

Investors may consider tilting their equity exposure toward value-centric and dividend-paying sectors, leveraging the improved earnings quality and lower relative valuations. Financials, particularly large regional banks with robust capital ratios, offer attractive entry points. Similarly, the Industrial sector, benefiting from renewed capital expenditure cycles, presents opportunities for long-term compounding. Simultaneously, maintaining exposure to the defensive growth elements of the healthcare sector ensures portfolio resilience during potential market drawdowns.

The technology sector, while not leading the current rally, remains crucial. However, selection within tech should prioritize companies with strong free cash flow and realistic valuations, rather than those relying purely on speculative future growth. The market is becoming increasingly discerning, rewarding profitability over promise. Diversification across market capitalization is also key; while the S&P 500 is focused on large caps, mid-cap value stocks have historically outperformed during the middle stages of an economic expansion, a phase the US economy appears to be entering.

Ultimately, the move to 6871 is a testament to the market’s adaptability. It reflects a transition from a low-interest-rate, zero-cost-of-capital paradigm to one where capital is constrained and profitability is paramount. Portfolio construction should mirror this reality, emphasizing balance, quality, and a measured approach to risk.

| Key Factor/Metric | Market Implication/Analysis |

|---|---|

| S&P 500 Index Level | Reached 6871 points, marking a historical all-time high driven by broad market participation beyond the largest tech stocks. |

| Sector Leadership | Value stocks (Financials, Energy) and Healthcare are leading, signaling a rotation away from high-growth technology. |

| Value vs. Growth P/E Gap | The valuation gap has narrowed by 18% year-to-date, reflecting the attractiveness of established cash flows in a higher-rate environment. |

| US GDP Growth Projection | Projected at 2.1% for 2025, supporting the ‘soft landing’ narrative and underpinning cyclical sector performance. |

Frequently Asked Questions about S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally

Value stocks, often tied to cyclical sectors like Financials and Energy, benefit from robust economic expansion and stable interest rates. Higher rates reduce the present value of future earnings, making current cash flows of value companies more appealing relative to high-multiple growth stocks.

The healthcare rally is driven by strong innovation, particularly in biotechnology and pharmaceuticals, exemplified by high demand for novel treatments. Additionally, the sector’s defensive characteristics provide stability, attracting capital seeking lower volatility and reliable earnings growth.

The S&P 500’s forward P/E ratio of 20.5x is higher than historical averages, suggesting valuation risks. However, the breadth of the rally and strong corporate earnings outside of tech mitigate some concerns, but investors should remain cautious about growth projections.

Investors may consider increasing exposure to undervalued cyclical sectors like Industrials and Materials and maintaining a core allocation to resilient healthcare names. Diversification is key; avoid overconcentration in previously dominant, high-multiple technology segments that are now lagging.

The primary risk is a potential monetary policy error, specifically if inflation re-accelerates, forcing the Federal Reserve to resume aggressive rate hikes. This scenario would severely undermine the valuations of both value and growth stocks, triggering a broad market correction.

The bottom line: sustainability and selectivity

The ascent of the S&P 500 to 6871 points is a powerful indicator of market confidence, rooted in a healthier, more diversified foundation than previous technology-led peaks. The leadership provided by value stocks, underpinned by economic resilience and strong corporate profitability in cyclical sectors, combined with the defensive stability and innovation within healthcare, suggests a more sustainable phase of the bull market. However, the elevated aggregate valuation and persistent macroeconomic uncertainties, particularly surrounding inflation and interest rate policy, demand selectivity. Institutional money managers are shifting their focus from simple growth narratives to companies demonstrating tangible earnings quality and superior operational execution. Moving forward, market participants must closely monitor Q4 2024 earnings reports for signs of margin pressure and watch Federal Reserve communications for any deviation from the current interest rate trajectory. The future success of the S&P 500 Reaches 6871 Points: Value Stocks and Healthcare Leading Rally hinges on the continuation of the ‘soft landing’ narrative and the sustained outperformance of these newly dominant sectors.