Mortgage Rates at 5.99%: Refinance Analysis and Market Outlook

The 5.99% mortgage rate environment necessitates a rigorous analysis of individual financial metrics, specifically comparing the potential monthly savings against the total cost of closing, to determine the precise breakeven point for any refinancing transaction.

The stabilization of the 30-year fixed mortgage average near the 6.0% psychological threshold—specifically, Mortgage Rates at 5.99%: Is Now the Time to Refinance Your Home?—marks a critical inflection point for millions of homeowners across the United States. This rate drop, often driven by shifts in the 10-year Treasury yield and evolving Federal Reserve expectations, compels a fresh evaluation of refinancing feasibility. For those with existing mortgages above 7.0%, the 5.99% offer represents a substantial potential reduction in monthly housing expenses, demanding immediate, data-driven analysis.

Understanding the Economic Context of 5.99% Rates

The current mortgage rate landscape near 5.99% is not an isolated event; it is a direct consequence of broader macroeconomic trends, specifically the Federal Reserve’s pivot toward potential future rate cuts and a corresponding moderation in inflation data. The 30-year fixed mortgage rate generally tracks the 10-year Treasury yield, plus a spread reflecting risk and operational costs. When the market prices in fewer aggressive rate hikes—or anticipates cuts—Treasury yields decline, pulling mortgage rates down.

As of Q4 2024, the Consumer Price Index (CPI) has shown annualized growth decelerating toward 3.2%, down from its 9.1% peak in mid-2022. This disinflationary trend has given the bond market confidence that the Federal Open Market Committee (FOMC) may ease policy in the coming quarters. This anticipation is the primary driver allowing lenders to offer conventional 30-year fixed rate mortgages below the 6.0% mark. For homeowners, this signals a temporary window of opportunity that is highly sensitive to incoming economic data, particularly employment reports and core inflation figures.

The Relationship Between Fed Policy and Mortgage Spreads

While the Fed does not directly set mortgage rates, its control over the short-term Federal Funds Rate profoundly influences the long-term borrowing costs through market expectations. Historically, the spread between the 10-year Treasury yield and the 30-year fixed mortgage rate averages around 170 basis points (bps). During periods of high economic uncertainty or volatility in the mortgage-backed securities (MBS) market, this spread widens. When rates stabilize and market liquidity improves, the spread tends to tighten, offering better rates to consumers.

- Market Volatility: Elevated volatility often pushes the mortgage spread wider, meaning consumers pay more relative to the underlying Treasury yield.

- Inflation Outlook: A sustained decline in inflation expectations typically lowers the 10-year Treasury yield, which is the foundational benchmark for the 30-year mortgage.

- FOMC Guidance: Dovish signals from the FOMC regarding future policy directly influence bond traders, leading to lower yields and, consequently, lower mortgage rates.

- MBS Demand: Strong institutional demand for Mortgage-Backed Securities helps keep the cost of lending down, contributing to competitive rate offerings like 5.99%.

The current 5.99% rate indicates that market participants are pricing in a high probability of at least 50 basis points of Fed rate cuts within the next 12 months, according to consensus estimates from major financial institutions like Goldman Sachs and JPMorgan Chase as of the start of the year. Any deviation from this expected path—such as unexpectedly strong jobs growth or a rebound in core inflation—could quickly push rates back above 6.5%, underscoring the time-sensitive nature of the current rate environment.

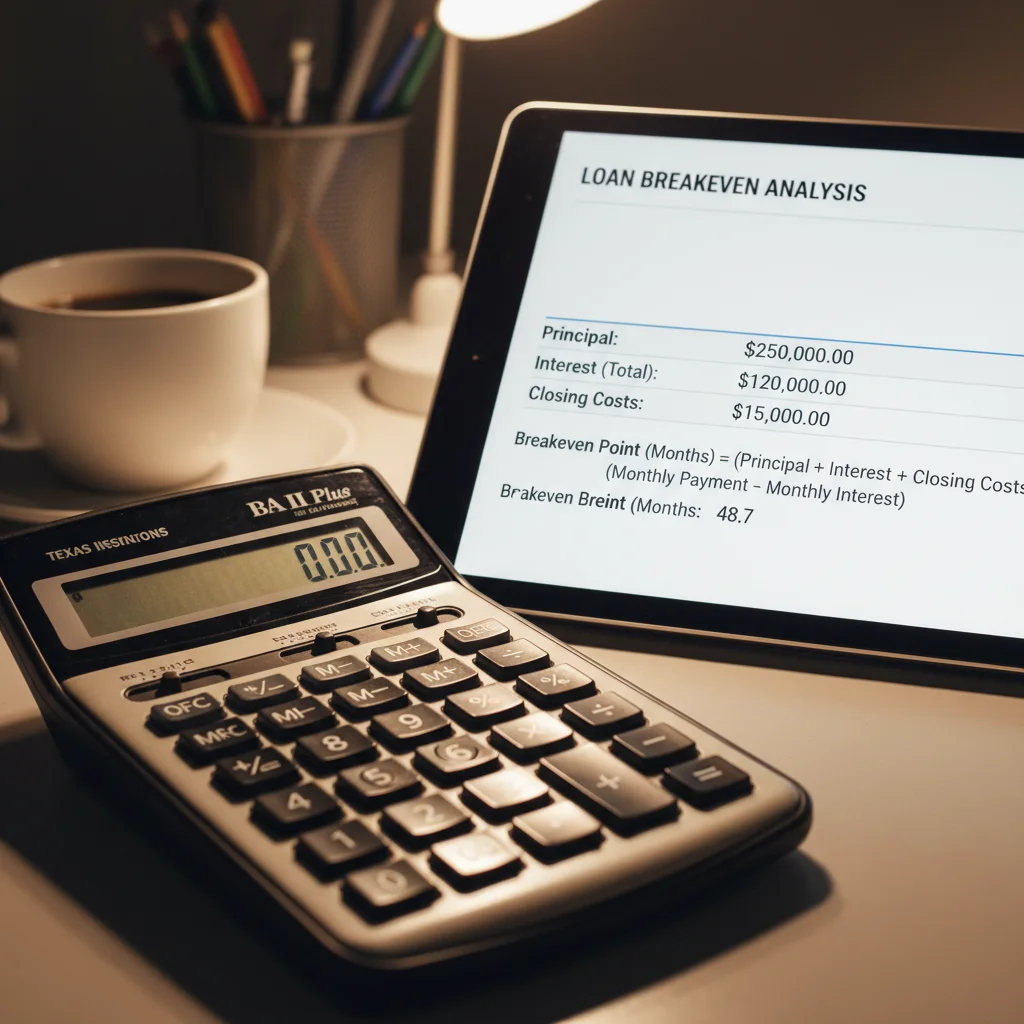

Calculating the Refinance Breakeven Point

The most critical component of the refinancing decision is the calculation of the breakeven point: the time required for the monthly savings from the lower rate to offset the upfront closing costs. Financial prudence dictates that a refinance should only be executed if the homeowner plans to remain in the property long enough to pass this threshold. Refinancing is not free; typical closing costs in the United States average between 2% and 5% of the loan principal, encompassing appraisal fees, title insurance, and origination charges.

Consider a hypothetical homeowner with an outstanding principal of $400,000 at a current rate of 7.5% and 25 years remaining. Refinancing to 5.99% reduces the monthly principal and interest payment. However, if closing costs total $8,000 (2.0% of the loan), the homeowner must calculate how many months of savings are needed to recover that $8,000 expenditure.

Methodology for Determining Net Present Value (NPV)

While the simple breakeven calculation (Total Costs / Monthly Savings) provides a quick estimate, sophisticated financial analysis requires considering the Net Present Value (NPV) of the transaction. NPV accounts for the time value of money, recognizing that a dollar saved today is worth more than a dollar saved in ten years. Analysts typically discount the future cash flows (monthly savings) back to the present using an appropriate discount rate, often the new lower mortgage rate itself.

- Monthly Savings Calculation: Determine the difference in the Principal and Interest (P&I) payment between the existing loan and the new 5.99% loan.

- Total Closing Costs: Accurately itemize all non-recurring and recurring closing costs, ensuring no fees are overlooked.

- Breakeven Period: Divide the Total Closing Costs by the Monthly Savings. If this resulting number of months exceeds the homeowner’s anticipated tenure in the home, the refinance may not be justifiable.

- Discount Rate Consideration: For a rigorous analysis, factor in an appropriate discount rate to calculate the true NPV of the transaction over the expected holding period.

For the $400,000 loan example, a drop from 7.5% to 5.99% on a 30-year term (assuming a reset of the term) could generate savings of approximately $375 per month. With $8,000 in closing costs, the simple breakeven point is roughly 21.3 months ($8,000 / $375). If the homeowner expects to move within 18 months, the transaction results in a net financial loss, regardless of the lower interest rate. This quantitative approach is paramount, overriding the temptation of securing a lower nominal rate without regard for transaction costs.

The Impact of Loan Term and Amortization Schedules

Refinancing at 5.99% often involves resetting the loan term, typically back to 30 years, which extends the amortization schedule and increases the total interest paid over the life of the loan, even if the rate is lower. Conversely, refinancing into a shorter term, such as a 15-year fixed mortgage, can significantly reduce the total interest burden but results in a substantially higher monthly payment. The decision hinges on the homeowner’s cash flow needs versus their long-term wealth accumulation goals.

Homeowners who originally secured loans during the hyper-low rate environment (e.g., 2020-2021) at rates below 4.0% are highly unlikely to benefit from a 5.99% rate, as the increase in interest expense would far outweigh any marginal benefit. The ideal candidates for the current 5.99% rate are those who purchased or refinanced during the peak rate periods of 2022 or 2023, when rates frequently exceeded 6.5% and sometimes touched 8.0%, according to Freddie Mac data.

Analyzing the 15-Year vs. 30-Year Refinance Trade-off

The choice between a 15-year and a 30-year term involves a direct trade-off between monthly liquidity and total cost. A $300,000 loan at 5.99% over 30 years results in a principal and interest payment of approximately $1,797. The same loan amount over 15 years, often available at a slightly lower rate (e.g., 5.50%), would see the P&I payment jump to about $2,452. While the 15-year option saves tens of thousands in total interest, the increased monthly obligation must be sustainable within the household budget.

- 30-Year Refinance: Maximizes monthly cash flow savings; suitable for homeowners prioritizing liquidity or those planning to allocate extra cash toward higher-yielding investments (e.g., equity markets).

- 15-Year Refinance: Accelerates equity buildup and significantly reduces total lifetime interest paid; appropriate for homeowners with stable, high incomes seeking aggressive debt reduction.

- Cash-Out Refinancing: Refinancing at 5.99% may also be attractive for those seeking to tap into home equity at a rate significantly lower than credit card debt (average 21.47% as of Q3 2024, per Fed data) or personal loans.

A critical consideration is the remaining term on the existing loan. If a homeowner is 10 years into a 30-year mortgage, resetting the clock back to 30 years, even at 5.99%, adds 10 years of interest payments. In such cases, financial advisors often recommend exploring a 20-year or 15-year refinance option to maintain a similar or accelerated amortization schedule, mitigating the overall cost of the transaction.

The Role of Credit Score and Loan-to-Value (LTV)

The 5.99% rate advertised by lenders is generally reserved for borrowers with pristine financial profiles. Lenders use specific metrics—primarily the FICO credit score and the Loan-to-Value (LTV) ratio—to determine eligibility and the exact rate offered. A borrower with a credit score below 740 may find that their actual rate is 6.25% or higher, diminishing the benefit of refinancing.

LTV, the ratio of the loan amount to the home’s appraised value, is equally important. Borrowers with LTVs below 80% often secure the most favorable terms, avoiding the cost of Private Mortgage Insurance (PMI) and qualifying for lower interest rates due to reduced risk for the lender. Rapid home price appreciation in many U.S. markets over the past three years means many homeowners have significantly lower LTVs than when they initially purchased.

Fannie Mae and Freddie Mac Conforming Loan Requirements

The vast majority of 30-year fixed mortgages are conforming loans, meaning they adhere to the standards set by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). These agencies dictate the maximum loan size and minimum credit qualifications necessary for the most competitive rates. For a borrower to achieve a rate near 5.99%, the following criteria are typically necessary:

- FICO Score: Generally 740 or above. Scores below 680 often result in rates exceeding 7.0%.

- LTV Ratio: Ideally 80% or less. LTVs above 90% significantly increase risk and cost, sometimes requiring PMI or a higher rate premium.

- Debt-to-Income (DTI) Ratio: Total monthly debt payments typically must not exceed 43% of gross monthly income, though lower DTIs (sub-36%) are preferred for the best rates.

- Appraisal Value: The current market appraisal must support the desired LTV. If the home appraisal comes in lower than expected, the homeowner may need to inject cash to meet the desired LTV threshold.

It is crucial for homeowners considering a refinance to obtain a current credit report and score and to estimate their home’s value accurately before applying. A preliminary qualification check reveals the true rate available, preventing disappointment and wasted closing cost expenditures. The difference between 5.99% and 6.25% on a $350,000 loan over 30 years amounts to over $50 in monthly payments, illustrating the financial impact of marginal differences in credit qualification.

Forecasting Future Rate Movements: The Uncertainty Factor

While 5.99% is attractive relative to recent highs, the decision to refinance now involves a calculation of opportunity cost: should one wait for potential further rate drops? The future trajectory of mortgage rates is inextricably linked to the Federal Reserve’s battle against inflation and the subsequent normalization of the yield curve.

Economists at institutions like PIMCO and BlackRock suggest that if inflation continues its downward path toward the Fed’s 2.0% target, rates could eventually settle in the mid-5.0% range by late 2025. However, this forecast is tempered by persistent risks, including geopolitical instability and potential supply chain disruptions, which could reignite inflationary pressures and force the Fed to maintain a higher-for-longer stance.

The Risk of Waiting for Lower Rates

Waiting for a rate below 5.5% carries the risk that economic data strengthens unexpectedly, causing the 10-year Treasury yield to reverse course and push mortgage rates back up. This phenomenon, known as market overshooting, occurred in early 2023 when strong employment data briefly stalled the expected rate decline. Market participants must weigh the potential for an additional 25-50 bps savings against the risk of losing the current 5.99% opportunity entirely.

- Upside Risk: If inflation proves sticky (e.g., remaining above 3.0% annualized), the Fed may delay cuts, stabilizing or increasing long-term rates.

- Downside Risk: A sudden economic slowdown or recession could trigger aggressive Fed cuts, pushing rates lower, potentially into the low 5.0% range.

- The Rate Lock Dilemma: Lenders typically offer rate locks for 30 to 60 days. Securing the 5.99% rate now provides certainty, protecting the borrower from adverse market movements during the closing process.

For homeowners whose current rate is 7.0% or higher, the immediate savings at 5.99% are substantial enough to justify the transaction, even if rates drop slightly further later. Financial analysts often recommend securing the current beneficial rate rather than gambling on marginal future improvements, particularly when the breakeven point is less than two years. The financial benefit of immediate lower payments often outweighs the speculative benefit of a potentially lower rate in six to nine months.

Alternative Strategies: HELOCs and Second Mortgages

For many homeowners, the goal is not necessarily to reduce the primary mortgage interest rate, but rather to access home equity to fund large expenses, debt consolidation, or investments. While a full refinance to 5.99% achieves this via a cash-out option, alternative instruments like Home Equity Lines of Credit (HELOCs) and Second Mortgages (Home Equity Loans) offer ways to tap equity without disturbing an existing low-rate primary mortgage (e.g., a 3.5% loan from 2021).

HELOCs and second mortgages operate differently. Second mortgages are fixed-rate, lump-sum loans, while HELOCs offer revolving credit, typically tied to the Prime Rate plus a margin, making them variable-rate products. Given the current high level of the Federal Funds Rate (which influences Prime Rate), HELOCs currently carry rates significantly higher than 5.99%, often exceeding 8.0% as of late 2024.

Comparing Cash-Out Refinancing vs. Home Equity Products

The primary advantage of a cash-out refinance at 5.99% is the ability to lock in a fixed, relatively low rate for the entirety of the funds borrowed. This is particularly appealing for large, long-term funding needs, such as major home renovations or paying off high-interest consumer debt. However, it means sacrificing the existing low rate on the primary loan balance.

- Cash-Out Refinance (5.99% Fixed): Best for replacing a high-rate primary mortgage and needing a large, predictable sum for long-term use. All funds are locked into the low rate.

- Home Equity Loan (Fixed Rate, e.g., 7.5%): Suitable for homeowners who have a primary mortgage below 5.0% and need a predictable, single-sum loan, accepting a higher second-lien rate.

- HELOC (Variable Rate, e.g., Prime + 1%): Recommended for flexible, smaller, or intermittent borrowing needs, but exposes the borrower to future rate hikes as the rate fluctuates with the Prime Rate.

In the context of the 5.99% offer, a cash-out refinance becomes highly compelling for those whose current primary mortgage rate is already high (above 6.5%). By consolidating the existing debt and accessing equity at 5.99%, the homeowner achieves both a lower overall borrowing cost and improved liquidity. Conversely, if the current mortgage is 4.0%, taking out a second mortgage at 7.5% might be preferable to raising the rate on the full primary balance to 5.99%.

The Documentation and Closing Process Efficiency

The efficiency of the refinancing process significantly affects the overall cost and feasibility of securing the Mortgage Rates Refinance Decision. Delays in closing can lead to the expiration of a favorable rate lock, forcing the borrower to accept a higher prevailing rate. Lenders are currently experiencing high application volumes due to the attractive 5.99% rate, which can slow processing times.

To mitigate delays, borrowers must ensure rapid and accurate submission of all required financial documentation. This includes W-2 forms, recent pay stubs, bank statements, and tax returns for the previous two years. Any discrepancies or incomplete documentation are the primary causes of closing timeline extensions.

Streamlining the Refinance Application

Digitalization has streamlined much of the initial application phase, but the underwriting process remains rigorous, particularly regarding appraisal and title review. Homeowners should actively monitor the process and communicate proactively with their loan officer to address contingencies immediately. The goal is to close the loan within the rate lock period, typically 30 to 45 days, to guarantee the 5.99% rate.

- Pre-Approval: Obtain a conditional pre-approval that clearly states the rate and closing cost estimates before paying for an appraisal.

- Appraisal Timing: Schedule the appraisal immediately upon application, as this is often the longest external dependency in the closing process.

- Closing Costs Negotiation: While some fees (like title insurance) are fixed, others (origination fees, junk fees) can be negotiated. Borrowers should compare Loan Estimates (LEs) from multiple lenders to ensure competitiveness.

- Escrow Management: Understand how existing escrow balances will be managed and transferred or refunded upon closing, avoiding unexpected cash flow disruptions.

Financial institutions often offer “no-cost” refinances, where the lender pays the closing costs in exchange for a slightly higher interest rate (e.g., 6.125% instead of 5.99%). For homeowners with a very short expected tenure in the home (less than two years), the no-cost option eliminates the breakeven calculation entirely, making it immediately beneficial due to the lower monthly payment, despite the marginally higher rate. This strategy is a viable alternative for minimizing upfront cash outflow.

| Key Factor/Metric | Market Implication/Analysis |

|---|---|

| Current Mortgage Rate > 7.0% | Refinancing to 5.99% is highly likely to be financially beneficial, provided the breakeven point is met within the anticipated home tenure (ideally < 24 months). |

| Total Closing Costs (2% – 5% of Loan) | Must be fully offset by monthly savings. High costs extend the breakeven period, potentially negating the advantage of the lower rate. |

| Federal Reserve Policy Outlook | Anticipated rate cuts support continued stability or marginal declines in mortgage rates, but waiting risks a potential reversal if inflation proves persistent. |

| Borrower Credit Score (FICO > 740) | Essential for qualifying for the advertised 5.99% rate. Lower scores attract rate premiums, reducing the net financial benefit of the transaction. |

Frequently Asked Questions about Refinancing at 5.99%

The ideal candidate holds a current mortgage rate above 6.75%, has a stable income, a FICO score exceeding 740, and plans to remain in their home for at least 24 months to surpass the typical breakeven point on closing costs.

The true cost includes all non-recurring closing costs, such as origination fees, appraisal costs, and title insurance, which typically range from 2% to 5% of the loan principal. These costs must be recovered through monthly savings.

Yes, if your anticipated tenure in the home is short (less than two years), a no-cost option eliminates the upfront cash outlay and makes the refinance immediately profitable through lower monthly payments, despite a marginally higher rate.

The main risk is that unexpected positive economic data, like sustained low unemployment, could prompt the Federal Reserve to hold rates higher, causing the 10-year Treasury yield to rise and mortgage rates to potentially climb back over 6.5%.

Refinancing to a new 30-year term resets the amortization schedule, meaning you pay interest for longer. To mitigate this, consider a 15-year or 20-year term if your cash flow permits, significantly reducing the total lifetime interest expense.

The Bottom Line

The emergence of 30-year fixed Mortgage Rates Refinance Decision near 5.99% represents a crucial opportunity for a specific segment of the housing market—those who secured loans during the high-rate cycle of 2022-2023. This is not a universal call to action; homeowners with rates below 6.0% or those who have already paid down significant portions of their loan should approach refinancing with extreme caution, prioritizing the preservation of their existing lower interest rate and shorter amortization schedule.

For qualifying candidates, the 5.99% rate provides a tangible reduction in housing costs and a necessary hedge against future market volatility. The decision must be grounded in an objective, quantitative analysis, specifically focusing on the breakeven point relative to expected home tenure. As the Federal Reserve navigates the final stages of its inflation fight, mortgage rates remain hypersensitive to economic indicators. Market participants should monitor incoming CPI and employment data closely, understanding that the window for rates below 6.0% may be transient. Securing the 5.99% rate now offers certainty and immediate financial relief, often outweighing the speculative potential of marginal future rate drops.