Mixed December Data Tests Record-High Rally’s Sustainability

The convergence of robust labor market figures, specifically non-farm payrolls exceeding forecasts by 50,000, and decelerating core inflation metrics in December created a pivotal moment, testing the endurance of the current equity market rally amid re-evaluation of the Federal Reserve’s rate path.

The final month of the calendar year often consolidates market trends, yet December 2024 delivered a complex, contradictory economic narrative that placed the record-high equity surge under immediate scrutiny. The juxtaposition of a surprisingly strong labor market, evidenced by non-farm payrolls (NFP) growth, against continued deceleration in the core Personal Consumption Expenditures (PCE) inflation index, has created a definitive test for the sustainability of the current rally. Investors are now actively parsing this mixed December data to recalibrate expectations for Federal Reserve monetary policy in Q1, particularly concerning the timing and magnitude of potential rate cuts, which has been the primary catalyst for the recent ascent in the S&P 500 and Nasdaq Composite.

The Labor Market Paradox: Strength Amid Easing Price Pressure

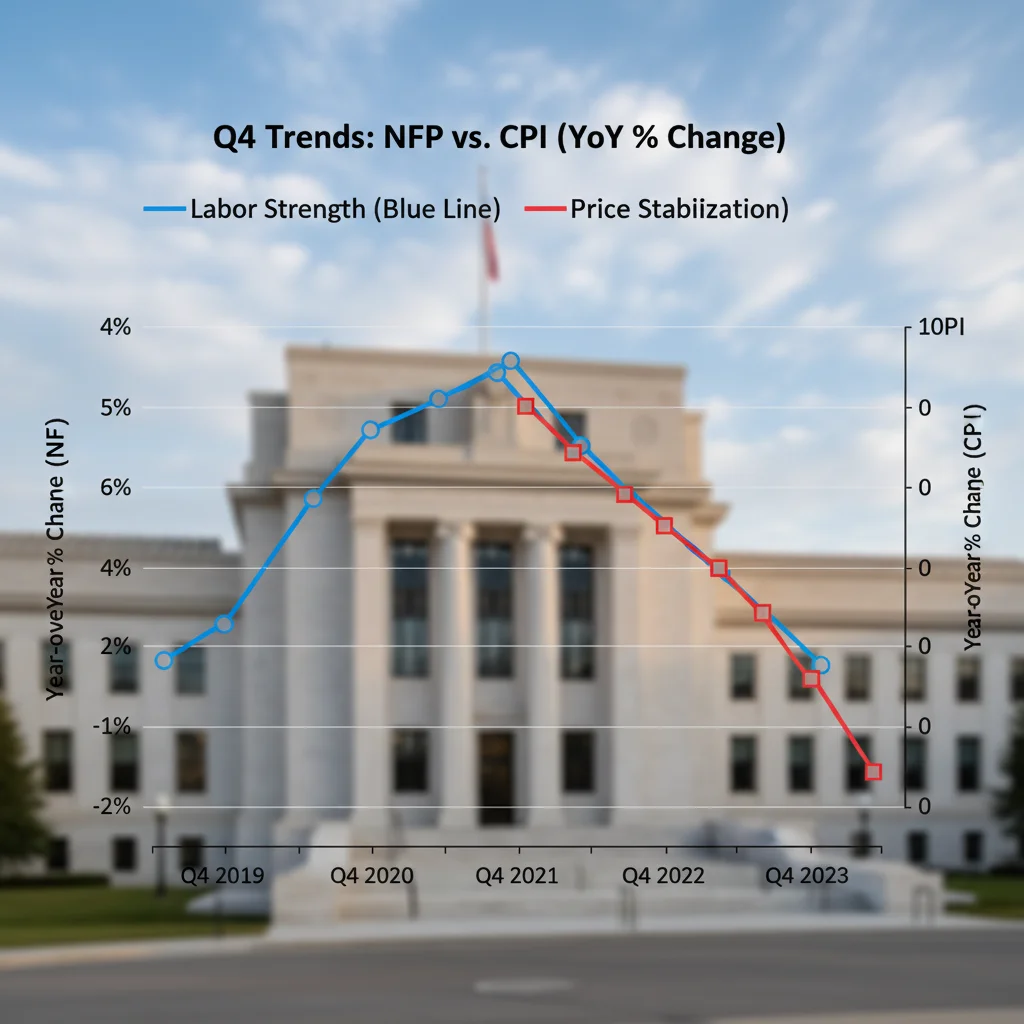

December’s employment figures were arguably the most confounding element of the month’s economic releases. While the market had largely priced in a gradual softening of the labor market, the Bureau of Labor Statistics reported NFP growth of 216,000 jobs, significantly surpassing the consensus forecast of 165,000. This unexpected strength suggested underlying economic resilience that challenges the narrative of an imminent, growth-slowing recession. However, this robust job creation occurred simultaneously with the core PCE—the Fed’s preferred inflation gauge—ticking down to 2.9% year-over-year, marking the first sub-3.0% reading in nearly three years, according to the Department of Commerce.

This labor market paradox complicates the Fed’s dual mandate. Strong employment typically implies sustained wage growth pressures, which should, in theory, impede the final leg of the inflation fight. Yet, the data suggests that productivity gains or shifts in labor participation might be absorbing this wage pressure without reigniting consumer price growth. This divergence forces a critical re-evaluation of the Phillips curve relationship, which posits an inverse link between unemployment and inflation, a relationship that appears historically weak in the current cycle.

Wage Growth and Participation Rates

A deeper dive into the December labor report reveals nuanced details that temper the headline NFP number’s hawkish implications. Average hourly earnings (AHE) increased by 0.4% month-over-month, higher than the 0.3% expected, pushing the year-over-year figure to 4.1%. While still elevated, the annual rate of AHE growth has been steadily cooling from its peak near 5.6% in 2022. Concurrently, the labor force participation rate remained largely flat at 62.5%. This stability, coupled with strong hiring, suggests demand remains high, particularly in sectors like healthcare and government, which added 38,000 and 22,000 jobs, respectively.

- NFP Total: 216,000 jobs added, significantly above the 165,000 forecast, indicating unexpected economic momentum.

- Average Hourly Earnings (YoY): 4.1% increase, signaling sustained, albeit slowing, wage inflation pressure.

- Unemployment Rate: Held steady at 3.7%, confirming tight labor conditions despite inflation cooling.

- Sectoral Strength: Continued robust hiring in services sectors, particularly health and education, offsetting slight declines in temporary help services.

The market implication of this employment strength is twofold: first, it reduces the probability of a hard landing, supporting corporate revenues; second, it raises the bar for Fed rate cuts, pushing back the expected timing of the first cut deeper into the year. Analysts at Goldman Sachs noted in a January research report that the NFP data increased their projected Q1 GDP growth rate from 1.8% to 2.1%, attributing the revision primarily to sustained consumer spending driven by employment gains.

Inflationary Headwinds Retreat: The PCE Deceleration

While the job market showed unexpected vigor, the inflation side provided the dovish counterpoint, fueling the narrative of a successful disinflationary process. The core PCE index, which strips out volatile food and energy components, registered a 0.1% month-over-month increase in December, translating to the 2.9% year-over-year figure. This decline is critical because it brings the metric closer to the Fed’s 2.0% target, reinforcing the central bank’s confidence that inflation is under control, even if the employment picture remains hot. This particular data point has provided crucial support to the long-duration technology stocks that thrive on lower interest rate expectations.

The persistent decline in goods inflation played a significant role in this deceleration. Supply chain normalization has allowed prices for durable goods to moderate, and in some cases, decline outright. However, the stickiness of services inflation remains the primary concern. Housing services inflation, though expected to cool based on lagged rental data, remains elevated, and non-housing services inflation, closely tied to wage cost pressures, requires further observation. The December PCE report confirmed that the disinflationary trend is primarily driven by goods and easing energy costs, leaving the high-contact services sector as the final frontier in the battle against inflation.

The Impact on Treasury Yields and Rate Expectations

The conflicting labor and inflation data immediately injected volatility into the fixed-income market. Initially, the strong NFP report caused the 10-year Treasury yield to jump from 3.90% to 4.05% within hours, reflecting reduced probability of aggressive early-year rate cuts. However, the subsequent release of the soft PCE data helped anchor yields, bringing the 10-year back down to the 3.95% level by month-end. This oscillation underscores the market’s sensitivity to macroeconomic data and the ongoing debate over whether the Fed will prioritize employment stability or inflation targets.

- 10-Year Treasury Yield Volatility: A 15 basis point swing immediately following the NFP report, demonstrating rate cut sensitivity.

- Fed Funds Futures: Probability of a March rate cut dropped from 75% to 55% after NFP, only partially recovering after the PCE release.

- Real Rates: Maintained positive territory, suggesting monetary policy remains restrictive, even if nominal yields fluctuate.

The net effect of December’s mixed signals on yields is a flattening of the short end of the curve, as the market accepts that the Fed may hold the policy rate at its current restrictive level longer than previously expected. This ‘higher for longer’ mentality, reinforced by the strong labor data, provides a structural challenge to the high valuations currently supporting the major equity indices, particularly those reliant on low borrowing costs for future growth discounting.

Corporate Earnings Outlook: Navigating the Macro Divide

The divergence between labor strength and price cooling sets a complex backdrop for the upcoming Q4 corporate earnings season, which begins in earnest in January. Companies face a trade-off: strong consumer demand, implied by the NFP figures, supports top-line revenue growth, but persistent wage inflation (AHE at 4.1%) continues to squeeze profit margins. For the S&P 500 companies, FactSet projects a modest 2.5% year-over-year earnings growth for Q4, a conservative estimate reflecting margin compression concerns.

Sectors most exposed to labor costs, such as consumer discretionary services and transportation, are under particular pressure. Conversely, technology firms with high operational leverage and less reliance on direct labor input are expected to outperform. Microsoft and Alphabet, for instance, are anticipated to show margin expansion driven by efficiencies from AI integration, rather than volume growth alone. This bifurcation in corporate performance is a defining feature of the current economic environment, where labor market tightness acts as a selective filter for corporate profitability.

The Role of Inventory and Capital Expenditure

December data also provided insights into corporate behavior regarding inventory accumulation and capital expenditure (CapEx). Business inventory-to-sales ratios showed a slight uptick, suggesting some companies might be holding excess stock, a potential drag on Q1 production. Meanwhile, durable goods orders, a proxy for future CapEx, showed a marginal sequential decline of 0.5%, according to the Census Bureau. This cautious CapEx environment suggests that despite the strong NFP numbers, corporate management teams remain hesitant to commit to large long-term investments, signaling underlying uncertainty about the medium-term economic outlook, perhaps influenced by geopolitical risks or sustained high real rates.

The mixed signals from December require investors to shift focus from purely macroeconomic indicators to microeconomic fundamentals during the earnings season. Companies demonstrating effective cost management, successful price pass-through, and strategic CapEx allocation are likely to be rewarded, irrespective of the broader macroeconomic volatility. The market is increasingly distinguishing between businesses that can navigate a high-cost environment and those that cannot, a necessary adjustment for maintaining the integrity of the record rally.

Sector Rotation and Market Leadership in Question

The record-high rally witnessed late in the year was heavily concentrated in the ‘Magnificent Seven’ technology stocks, fueled by excitement over AI and the expectation of rapid, deep rate cuts. The mixed December data, however, immediately challenged this high-beta leadership. Utilities and consumer staples, traditionally defensive sectors, saw relative outperformance in the first week of January, a classic sign of market participants hedging against economic uncertainty and adjusting to the ‘higher for longer’ rate narrative implied by the strong NFP report.

This potential sector rotation suggests a broadening of the market, moving away from narrow leadership. If the economy avoids a recession and inflation continues its slow descent toward 2.0%, cyclical sectors like financials and industrials, which benefit from sustained economic activity but are less sensitive to interest rate fluctuations than pure technology growth, may attract capital. Conversely, if the strong labor market forces the Fed to delay cuts significantly, the high-duration growth stocks could face downward pressure on their discounted future earnings.

The Technical Vulnerability of the Rally

From a technical analysis perspective, the S&P 500 closed December near its all-time high, having experienced one of the least volatile fourth quarters in recent memory. However, the recent price action following the mixed data has seen the index struggle to break decisively above its 52-week moving average resistance level. Analysts at Bank of America noted that the Relative Strength Index (RSI) for the S&P 500 remains in overbought territory (above 70) despite the recent volatility, suggesting that the market rally may be technically exhausted and susceptible to a correction if fundamental data, such as disappointing Q4 earnings, fails to justify current valuations. A 5% pullback from current levels would be a healthy, necessary consolidation to absorb the new reality of robust jobs and cooling prices.

- Defensive Sector Outperformance: Utilities (XLU) and Consumer Staples (XLP) saw early January gains, signaling risk-off sentiment.

- Technology Sector Risk: High-valuation tech stocks face increased scrutiny if the rate cut timeline is pushed back due to labor strength.

- Market Breadth: Investors are monitoring whether the rally broadens beyond the ‘Magnificent Seven’ to sustain momentum.

The technical indicators, combined with the fundamental data uncertainties, underscore the prevailing sentiment: while the bull market remains intact, its trajectory is now highly conditional on how Q1 economic data unfolds and how corporate America reports its profitability in a high-wage, disinflationary environment. The market is positioned at a crucial inflection point.

The Federal Reserve’s Policy Headaches and Forward Guidance

The Federal Reserve’s forward guidance, articulated in the December FOMC meeting minutes, emphasized data dependence. The mixed December data—strong jobs, soft inflation—presents a unique policy challenge that allows the Fed to maintain optionality without committing to an immediate pivot. Fed officials, including Governor Waller, have publicly stated that the central bank needs greater confidence that inflation is sustainably moving toward 2.0% before initiating rate cuts. The strong NFP print provides the Fed with the necessary cover to delay cuts, preventing a premature easing that could risk a re-acceleration of inflation.

The consensus among economists at institutions like JPMorgan Chase is that the Fed will likely wait until mid-year (June) before making the first 25 basis point cut, primarily due to the resilience of the labor market. This contrasts sharply with the market’s aggressive pricing of a March cut, creating a significant expectation gap that often fuels volatility in the short term. The Fed’s primary focus will shift from the headline inflation rate to the persistent components, specifically core services inflation excluding housing, which is highly correlated with wage pressures.

The Quantitative Tightening (QT) Component

Beyond the policy rate, the Fed’s ongoing Quantitative Tightening (QT) program, which continues to reduce the size of the balance sheet by allowing maturing Treasury and mortgage-backed securities to roll off, adds another layer of restrictive policy. While less visible than rate hikes, QT drains liquidity from the financial system, potentially offsetting some of the market euphoria driven by rate cut expectations. The effectiveness and appropriate duration of QT in the context of a decelerating, yet resilient, economy are now central to the policy debate.

The Fed’s communication strategy in Q1 will be paramount. Any indication that the labor market strength is overriding the disinflationary progress could lead to a rapid repricing of rate expectations, potentially triggering a significant market correction. Conversely, if the upcoming CPI and PPI reports confirm the downward trajectory of prices, the market may regain confidence in a soft landing, validating the current high equity valuations, despite the delay in rate cuts.

Global Economic Spillover and Currency Implications

The U.S. economic divergence, characterized by strong labor and cooling prices, has significant implications for global markets and currency valuation. While the Eurozone and China continue to face structural growth challenges, the U.S. economy appears relatively robust. This growth differential supports the U.S. Dollar Index (DXY), which saw renewed strength following the strong NFP report. A stronger dollar makes U.S. exports more expensive and reduces the repatriated value of international earnings for multinational corporations, creating an additional headwind for globally exposed S&P 500 companies.

Emerging markets (EM), particularly those reliant on dollar-denominated debt, are negatively affected by sustained dollar strength and higher-for-longer U.S. real rates. Capital flows tend to revert to the relative safety and higher yield of U.S. assets, increasing borrowing costs for EM economies. This dynamic underscores the interconnected nature of global finance, where U.S. domestic economic data immediately translates into global market conditions.

Commodity Price Sensitivity

Commodity markets, especially crude oil, reacted tepidly to the mixed data. While strong U.S. employment suggests robust demand for energy, the broader global growth concerns and the strong dollar acted as counterweights. West Texas Intermediate (WTI) crude oil prices remained range-bound between $70 and $75 per barrel throughout the period. This stability in commodity prices is a crucial factor supporting the disinflationary narrative, preventing a renewed surge in energy costs from derailing the Fed’s progress. However, geopolitical instability remains an unpredictable risk factor that could rapidly alter this equilibrium, forcing a quick reassessment of the inflation outlook.

In summary, the global market response to the mixed December data is one of cautious reassessment. The U.S. economy is performing better than its peers, but this strength complicates the monetary policy easing cycle, supporting the dollar and creating turbulence for emerging and commodity markets. Investors must monitor global central bank actions and international trade data as closely as domestic U.S. metrics to gauge the full impact of this domestic economic resilience.

| Key Metric/Factor | Market Implication/Analysis |

|---|---|

| Non-Farm Payrolls (NFP) | Stronger-than-expected +216,000 jobs reduces immediate recession risk but delays Fed rate cut expectations, supporting ‘higher for longer’ narrative. |

| Core PCE Inflation | Deceleration to 2.9% YoY validates the disinflationary trend, providing critical support for the soft-landing scenario and high-duration assets. |

| 10-Year Treasury Yield | Increased volatility and a push back toward 4.0% reflects market uncertainty regarding the timing of the first Fed rate cut, challenging equity valuations. |

| Corporate Earnings Growth (Q4) | Projected modest 2.5% growth reflects margin pressure from sustained high wage costs (4.1% AHE), requiring selective stock picking based on operational leverage. |

Frequently Asked Questions about Mixed December Data and Market Sustainability

The robust Non-Farm Payrolls (NFP) data reduces pressure on the Federal Reserve to cut rates immediately by confirming economic resilience. Analysts now largely expect the first rate cut to be delayed until mid-year (June) or later, allowing the Fed time to ensure inflation is firmly anchored at the 2.0% target before easing monetary policy.

The main risk is the potential for Q4 corporate earnings to disappoint due to margin compression. While strong demand exists, the sustained 4.1% year-over-year growth in average hourly earnings, suggested by the mixed December data, is squeezing profit margins, especially for labor-intensive companies, which may not meet current high stock valuations.

The ‘higher for longer’ environment poses a structural challenge to high-duration technology stocks, as their future earnings are discounted more heavily. Investors may consider diversifying into cyclical sectors like financials and industrials, which benefit from sustained economic growth and are relatively less sensitive to short-term interest rate fluctuations than pure growth plays.

The core PCE is the Fed’s preferred inflation metric, and its drop below 3.0% confirms that the disinflationary process is well underway. This significantly increases the probability of a soft landing, reassuring the market that the restrictive policy has worked, thereby mitigating fears of aggressive stagflation and supporting risk assets.

Investors should primarily monitor the Q4 earnings reports for signs of margin resilience and forward guidance on CapEx. Additionally, the month-over-month change in Core CPI and the ISM Services PMI data will be crucial for confirming whether the disinflationary trend continues and whether economic activity remains robust outside of the labor market.

The Bottom Line: Navigating Conditional Optimism

The mixed December data has effectively moved the market from a position of anticipatory certainty—where aggressive early rate cuts were widely priced in—to one of conditional optimism. The economy is demonstrably stronger than many models predicted, particularly in the labor market, yet the disinflationary progress remains intact. This combination is the hallmark of a potential soft landing, which, historically, is the most positive outcome for corporate earnings and equity valuations. However, the path forward is fraught with complexity. The primary tension lies between the market’s desire for immediate monetary easing and the Federal Reserve’s need for prudence in the face of persistent labor market strength.

For investors, the sustainability of the current record-high rally hinges not on continuous, broad-based ascent, but on selective performance. The market will reward companies that demonstrate pricing power and operational efficiency in managing high labor costs, rather than those reliant solely on volume growth or the expectation of cheap capital. The immediate focus shifts to the microeconomic reality revealed in Q4 earnings and the forward guidance provided by management teams. If corporate results validate the strong consumer demand implied by the NFP data without significant margin erosion, the rally can continue, albeit at a more moderate and volatile pace. Conversely, disappointing earnings could trigger the necessary technical correction that absorbs the conflicting macroeconomic signals. The coming months will test the market’s resilience and its ability to distinguish between economic strength and inflationary risk, making data dependency the ultimate investment mantra for the start of the year.